PARQOR is the handbook every media and technology executive needs to navigate the seismic shifts underway in the media business. Through in-depth analysis from a network of senior media and tech leaders, Andrew Rosen cuts through what's happening, highlights what it means and suggests where you should go next.

In Q4 2022, PARQOR will be focusing on four trends: this essay is on the theme, "Hollywood’s future lies in the creator economy, what happens next?"

I'm keen to connect with subscribers and readers on a free trial to learn more about you need from a subscription service. Click here to set up an appointment: https://calendly.com/andrew_parqor/30min

My general take on Netflix’s Q3 2022 earnings is that, for all their challenges, they still have over 223MM subscribers and are growing. The statement in the letter to shareholders that management is seeing “some encouraging signs of gameplay leading to higher retention” is interesting. The implication is that gaming has yet to drive growth, but is important to the Net Subscribers number because it reduces churn.

I’m fascinated by something Netflix Co-CEO Ted Sarandos said to close out this week’s earnings call:

“we have to continue to deliver enormous quality and scale. The volume of releasing that we're doing, it's not that we're putting out so much content, just dumping the content into the world. Actually, we're trying to super serve hundreds of millions of people with individual tastes and individual relationships with content and to do that at scale, something that's never been done before.”

It was his answer to a question asked to the entire Netflix team: ‘[what is the single most important thing for you and your teams to accomplish in your respective roles over the next 12 to 24 months”?

It’s one version of an answer to a question I asked on Wednesday: “As cord-cutting accelerates, what is the business of media if an app’s home page is more valuable than the content itself? Why have expensive production budgets for TV shows or movies when ultimately production value matters less than what is being presented when the user logs in?”

Key Takeaway

Netflix Co-CEO Ted Sarandos made a slid sales pitch to investors about why $17B is necessary in the age of the algorithm. But YouTube's growth makes the price tag increasingly seem steep.

Total words: 800

Total time reading: 3 minutes

Why the answer works

It seems unusual for Sarandos to be defending the rationale for Netflix’s content spend 15 years after the launch of its streaming service. Then again, they have had a rough year, shareholders are focused on profits, and therefore if content spend is not generating ROI then it should be cut.

It also seems unusual to be addressing the perception of Netflix’s quality in 2022. The answer is a bit of wordplay on Sarandos’s part (and Netflix investor relations, as in the video Sarandos is clearly reading this answer) that he is and is not defending quality as a standard. He’s defending it in the sense that the spend has an objective: to “super serve hundreds of millions of people with individual tastes and individual relationships with content.”

As I wrote on Wednesday, that has been something that both Hollywood and Wall Street have been struggling to comprehend: The internet “allows vast customization potential, in an economy premised for 200 years on industrial standardization.” Netflix believes the best content models focus on serving these various tastes and relationships with content.

But, he’s also conceding that these individual tastes and individual relationships with content don’t meet a single standard of quality, whether it’s a traditional Hollywood executive’s taste or a critic's or the wisdom of the crowds on Rotten Tomatoes. Beauty is in the eye of the beholder (but perhaps moreso the algorithm).

The problem with the answer

The optics of $17B is still a lot of money to be spending on content with only 6% year-over-year growth. It also does not help that a recession looms: what will $17B in content spend accomplish as household budgets decline?

Second, when considered against Monday’s essay “Netflix ($NFLX) May Not Have Any Answers For YouTube Shorts”, Sarandos’ answer leaves Netflix vulnerable to two critiques.

The first critique is that this answer does not discuss the competitive threat from YouTube Shorts and TikTok moving into Connected TV (CTV). As I wrote on Monday, after YouTube Shorts launches on YouTube’s CTV app “Netflix will be competing with multiple formats from YouTube, and has no obvious answers for Shorts.” or its creator economy model of faster, cheaper and sometimes better.

That points to a second critique: the optics of $17B seems exponentially expensive when compared to free. The optics change when considered in light of YouTube’s payments of $50B to creators over the past three years, or nearly $17B per year. It points to a more nuanced comparison of Netflix’s subscription model paying creators upfront based on an estimate of future results, or YouTube’s advertising model paying out creators based on performance.

Last, in light of Wednesday’s mailing, a third critique is the looming question of how Netflix’s soon-to-be-released Basic with ads tier can compete with YouTube. Sarandos promises investors - and implicitly advertisers - quality and scale. But, if the top 1% of YouTube creators in the Partner Program - or 2,000 content creators- produced 25 videos per year, that’s 50K videos per year. Netflix is estimated to have 17K titles in its library worldwide, or just over one-third of the volume of 0.1% of two million YouTube creators. And we can only imagine what the math will be as Shorts takes off as a format - it has 30B daily views and 1.5 billion logged-in viewers watching per month.

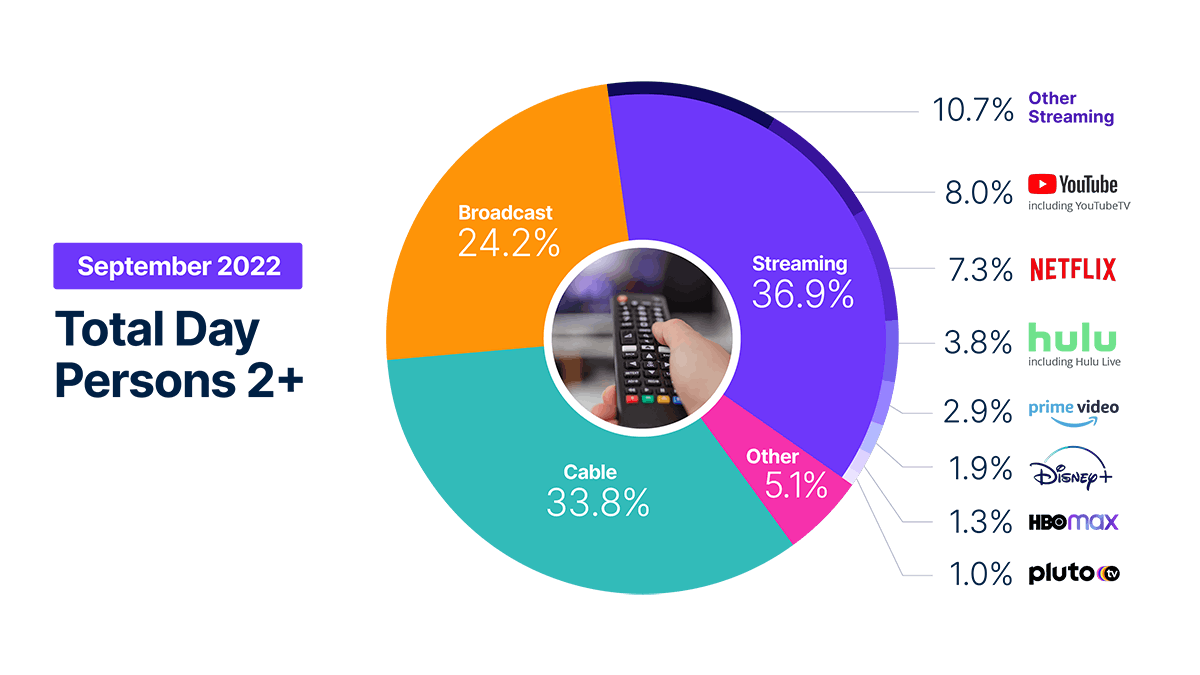

There are reasons for advertisers to buy ads from Netflix, but increasingly more reasons for them to buy ads from YouTube. According to figures from Nielsen’s The Gauge released last Thursday, YouTube captured 8% of TV viewing in September to Netflix’s 7.3%, after having tied at 7.6% in August.

Netflix now finds itself in an arms race with YouTube where YouTube seems to have an infinite supply of arms for which it pays a performance-based fee.