Correction: I wrote earlier "That story started with 10MM e-commerce advertisers moving their spend into CTV back in 2017, and with the objective of disrupting these 200 “retail-cartel” advertisers in the U.S. But the growth of CTV spend is now being driven by both sets of advertisers, and that is a story that is also not about advertising." But Connected TV spend started earlier in the decade, perhaps as early as Pluto TV's launch in 2013. That has been updated.

I realized something after writing about Upfronts over the past two weeks: this story of connected TV (CTV) ad spend is and also isn’t about advertising.

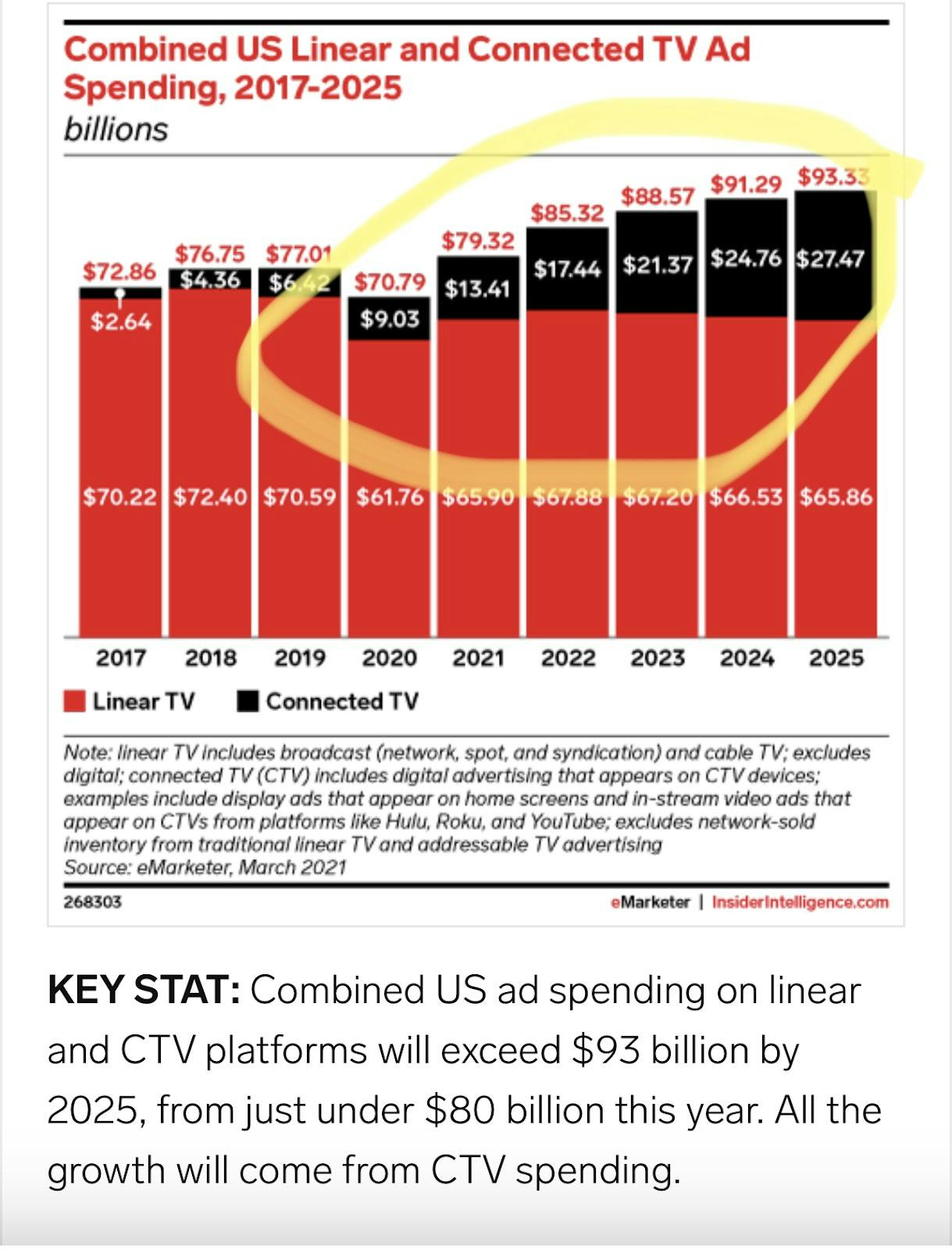

It is about advertising because it’s a story about how 200 “retail-cartel” advertisers are not adapting to a longer-term trend of shifting, declining audience demand for linear TV: projected linear spend is projected to stay flat for the next three years.

It’s also about Connected TV (CTV) advertising spend more than doubling over five years with a compound annual growth rate of 15.43% (highlighted above, though eMarketer now estimates total U.S. CTV ad spend will reach $18.89B this year, an 8% increase over the projection, above).

That story started with 10MM e-commerce advertisers moving their spend into CTV earlier last decade, and with the objective of disrupting these 200 “retail-cartel” advertisers in the U.S. But the growth of CTV spend is now being driven by both sets of advertisers, and that is a story that is also not about advertising.

As the growth of e-commerce sales continues to outpace U.S. retail sales, the data needs of both 200 “retail-cartel” advertisers and 10MM e-commerce advertisers are going to drive the evolution of linear and CTV advertising. All will increasingly rely on publishers to supply better data on consumers to improve the reach, segmentation, variability, and complexity of their marketing. But not all publishers will not be able to meet that evolving demand.

One solution from Accenture

A recent Accenture paper, Streaming’s Complex Consumer, reflects the “walled garden” problem that prevents publishers from doing so: with limited libraries and audiences locked into particular services, publishers are unable to understand consumer preferences holistically. In turn, the data publishers intend to sell to advertisers suffers from the same limitations, and as the Accenture report highlights, few appealing solutions.

The Accenture report leverages both consumer survey data and data from Whip Media (an enterprise software platform for worldwide content licensing) to better understand “today’s complicated consumer”. It’s worth reading the report (and listening to the podcast presentation of it) for how it highlights how consumers’ viewing habits differ across platforms and are not reflected in the recommendations they’re getting.

But, the value for the purposes of this mailing is the light it sheds on the problem of “walled gardens”, as IAB Executive Chairman Randall Rothenberg recently tweeted

…there will be many multiple “televisions,” each one striving to keep its own audience - an audience smaller than historical norms - locked in and blissfully unaware of those other televisions inhabiting other dimensions in different space-time continuums.

A previous Accenture report - Streaming’s next act - highlighted the impact of this problem both on publisher data and their recommendation engines:

Many algorithms generate recommendations based on an incomplete viewing history—and those recommendations can be wildly off base. Furthermore, the reliance on the algorithm to pitch consumers shows doesn’t allow consumers to tune the model, except through actual show selection.

Not surprisingly, a majority of consumers globally said they’d like to be able to take their profile from one service to another to better personalize content (56%); and they’d be happy to let a video-on-demand service know more about them to make recommendations more relevant to them (51%).

What makes Streaming’s Complex Consumer paper particularly notable is its proposed solutions to this problem of “walled gardens”:

“Quick wins” from acquiring and integrating viewing data from other platforms to help improve personalization and content recommendation algorithms

Medium-term solutions in developing priority consumer segments that are likely to find the content on offer more appealing, and using those segments to rethink content strategies and marketing.

Long-term solutions in a variety of strategies, including M&A, to enable consumers to carry their profile from one to the next for a more frictionless user experience.

In short, all roads point to publishers needing to figure out ways to tear down their walls and bundle.

The challenge(s) with bundling

If one subscribes to the argument that bundling subscription streaming services (SVODs) is the future of streaming - as Starz CEO Jeffrey Hirsch recently argued to Accenture’s competitor McKinsey - then one can also agree that from the above, a collective need across publishers for better consumer data to better serve consumers will drive SVOD bundling.

But, if one believes that ad-supported models are the future of streaming, then the implication is that a collective need across publishers for better consumer data to better serve advertisers will drive that bundling.

Also, neither outcome is mutually exclusive.

All said, one counterargument is that “we truly are in the early days of [Customer Data Platform] approaches across platforms” - as I argued last Friday’s $68B in Linear Ad Spend & Netflix, It's Early Days for CDPs in Media. Certain media businesses like Disney are savvier than their competition with their Customer Data Platforms (CDP).

Part of this is because they are PARQOR Hypothesis businesses - meaning, because they have (1) an Existing user base at scale, (2) multiple Avenues for monetizing the same IP, and (3) offline and online sales channels with those users, they have competitively robust first-party data to other streamers [1].

Also, top-scoring PARQOR Hypothesis businesses like Disney and Apple have a long history of building and operating multiple direct-to-consumer businesses around consumer data. But others like Warner Bros. Discovery and AMC Networks do not. So, even if competing publishers pursue the solutions Accenture recommends, those outcomes will always be suboptimal solutions for advertisers and consumers according to the PARQOR Hypothesis. [2]

The complexity of the problem may invite obvious solutions like bundles and mergers, as Accenture recommends. But, the PARQOR Hypothesis highlights why in most cases, those solutions may not be enough.

Footnotes

[1] Both this point and Accenture data raise an interesting implication about the PARQOR Hypothesis: Netflix has a large library, a sophisticated personalization algorithm and decades of consumer data, and therefore according to Accenture research it is better positioned than the competition to both serve consumer tastes and advertiser needs. But, according to the PARQOR Hypothesis, its data is suboptimal for advertisers because it lacks multiple Avenues to monetizing the same IP and offline sales channels.

There is also Amazon, which scores lower under the PARQOR Hypothesis: its entire business model is built around sophisticated understandings of its consumers (more shopping than content consumption).

[2] And, in the specific case of Warner Bros. Discovery, if it decides to bundle or merge with other services to improve consumer and advertiser data, the management team who best understands the solutions to this problem walked out the door in April after the merger closed (former CEO Jason Kilar and his team). And they were the exception in broadcast network teams.

Must-Read Monday AM Articles

* Parrot Analytics offers a primer on the existing bundles in streaming

* Insider has a good scoop on how much ads cost on 10 of the biggest streaming TV companies

* TiVo may have the best universal streaming guide, which lets you browse across services like HBO Max, Amazon Prime, and Hulu from a single menu

* Why advertising will never die

* An update on Nielsen and competition in the measurement marketplace (aka alternative measurement “currencies”) after Upfronts

The Vibe Shift

* Netflix’s test of password sharing in Peru is “a mess”, according to one report

* Warner Bros. is continuing its experimentation in the NFT (non-fungible token) business, with the characters from Looney Tunes being the next company IP to get the NFT treatment

* A good overview from Pitchfork of how the music business is and isn’t evolving around NFTS.

* How Nike has moved to capitalize on the excitement around new concepts such as the metaverse, NFTs, and web3

* Apple has enlisted Hollywood directors such as Jon Favreau to develop video content for a headset that it is expected to ship next year

* Lightshed’s Rich Greenfield discussed with Barrons how he thinks the media business changed during the pandemic

* Sony Pictures Entertainment chairman and CEO Tony Vinciquerra thinks “by far the greatest opportunity” in the market is the continued use of Sony’s IP, not only from its current film and TV library, but from the Sony Music and Playstation divisions as well.

Aggregator 2.0

* Variety VIP’s Kaare Eriksen argues that with Netflix producing original live-action versions of gaming IP, why not partner with a major gaming player for a perk that grants Netflix subscribers free access to these games? ($ - paywalled)

Sports & Streaming

* WWE shakes up leadership as it targets $100 million in sponsorship and brand revenue ($ - paywalled)

* Disney’s dilemma in India with cricket: millions of Disney+ subscribers, but viewers pay low rates while broadcast and streaming rights are likely to be expensive

* Netflix, ESPN, NBCUniversal, and Amazon are bidding on US Formula 1 rights

Creator Economy, Platforms & Transparency

* Spotify announced the creation of the Africa Podcast Grant to help highlight voices from the continent. The $100,000 fund is open to 10 creators.

* Forgotten pop stars, former Olympians, and washed-up tech entrepreneurs are all cashing in on China’s booming livestreaming scene

Original Content & “Genre Wars”

* A startup has acquired 18 Hispanic radio stations across 10 markets from TelevisaUnivision.

* Jeff Sagansky, a media investor and former President of CBS Entertainment and Sony Pictures Entertainment and former CEO of TriStar Pictures, spoke at a NATPE event and sounded “the alarm on the adverse impact" that the mass adoption of Netflix’s “cost plus” business model has had on profit participation

* “Which participants in the Streaming Wars will triumph... and which stand to lose everything?”

* Borys Kit of The Hollywood Reporter dives into Netflix’s new movie mandate of “Bigger. Better. Fewer.”, and the changes to the animation divisions. Also, why the return of Stranger Things is “only further proof "of Netflix's "unsustainability”

* Why Netflix has picked Poland as its new regional headquarters for the streamer’s operations across Central and Eastern Europe (CEE)

* Tosca Musk, Elon’s younger sister, is the force behind Passionflix, a streaming service dedicated to adaptations of romance novels and erotic fan fiction.

AVOD & Connected TV Marketplace

* Why slowing smart TV sales from rising prices and empty shelves have started to impact streaming services, including industry leader Netflix

* Why upfront presentations rarely change media buyers’ minds

* Major broadcast network linear TV took another hit for its prime-time entertainment series for the just-completed 2021-2022 TV season with high single- and double-digit-percentage viewing declines versus the previous season's results (free - sign-up required)

* Warner Bros. Discovery now has two new advertising options for streaming: Click-to-Contact focuses on how customers interact with ads, and Viewer’s Choice is centered on when customers see certain types of ads.

Other

* Candle Media made another purchase, this time Exile Content Studio, a producer of Spanish-language films, TV shows and podcasts.