Disney's OpenAI Deal Collapsed. It Is Suing Its Best Alternatives.

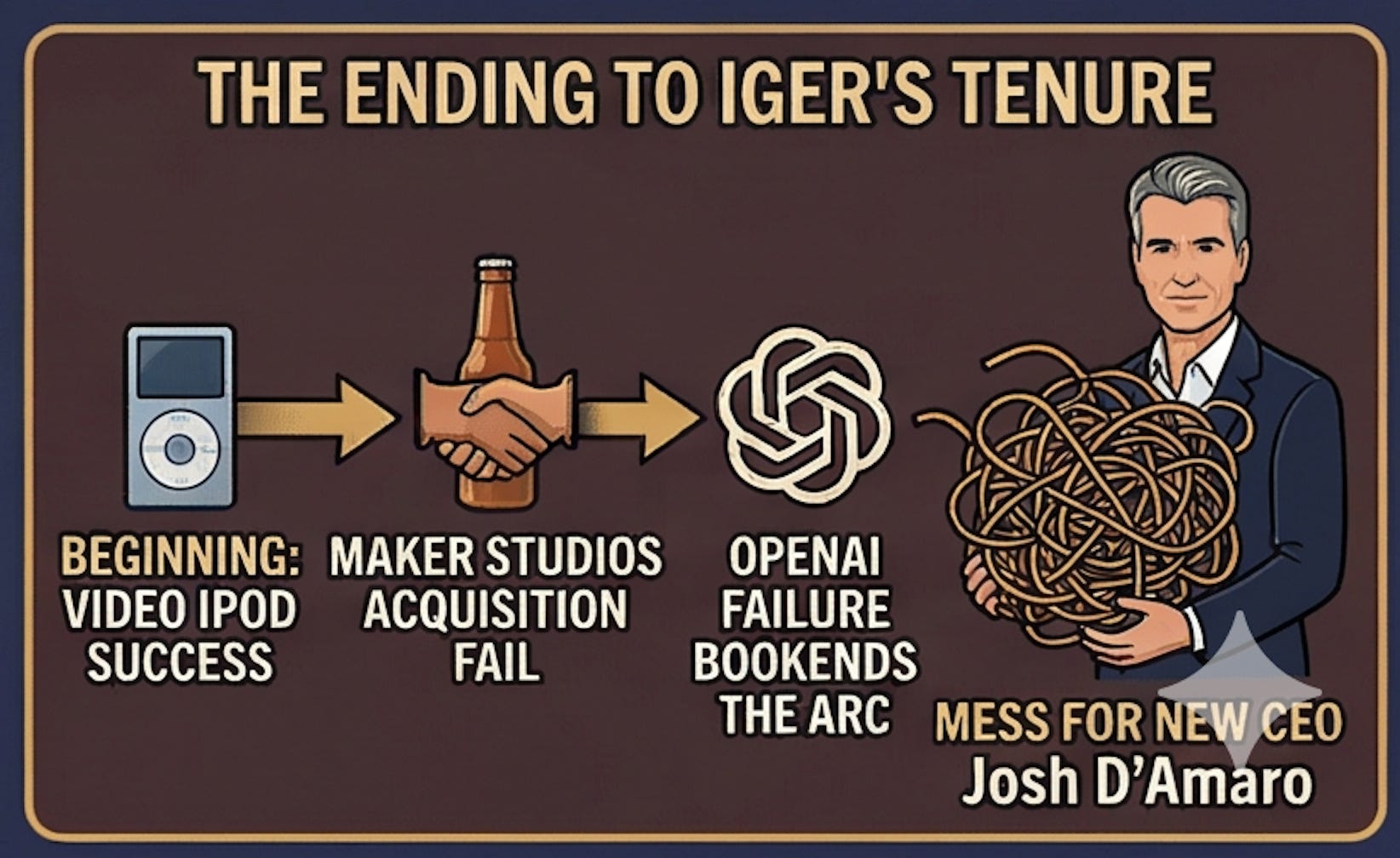

The OpenAI failure bookends the arc of Iger's failed strategy of leveraging Disney's IP over tech companies and leaves an unfortunate mess for new CEO Josh D'Amaro.

[Author’s Note: This essay is free for all subscribers.]

Disney’s $1 billion investment in OpenAI just unraveled in spectacular fashion, only three months after its signature and seven business days after former CEO Robert Iger stepped down. OpenAI announced it will discontinue Sora in the consumer app and API, and Disney announced it will seek other platforms as partners.

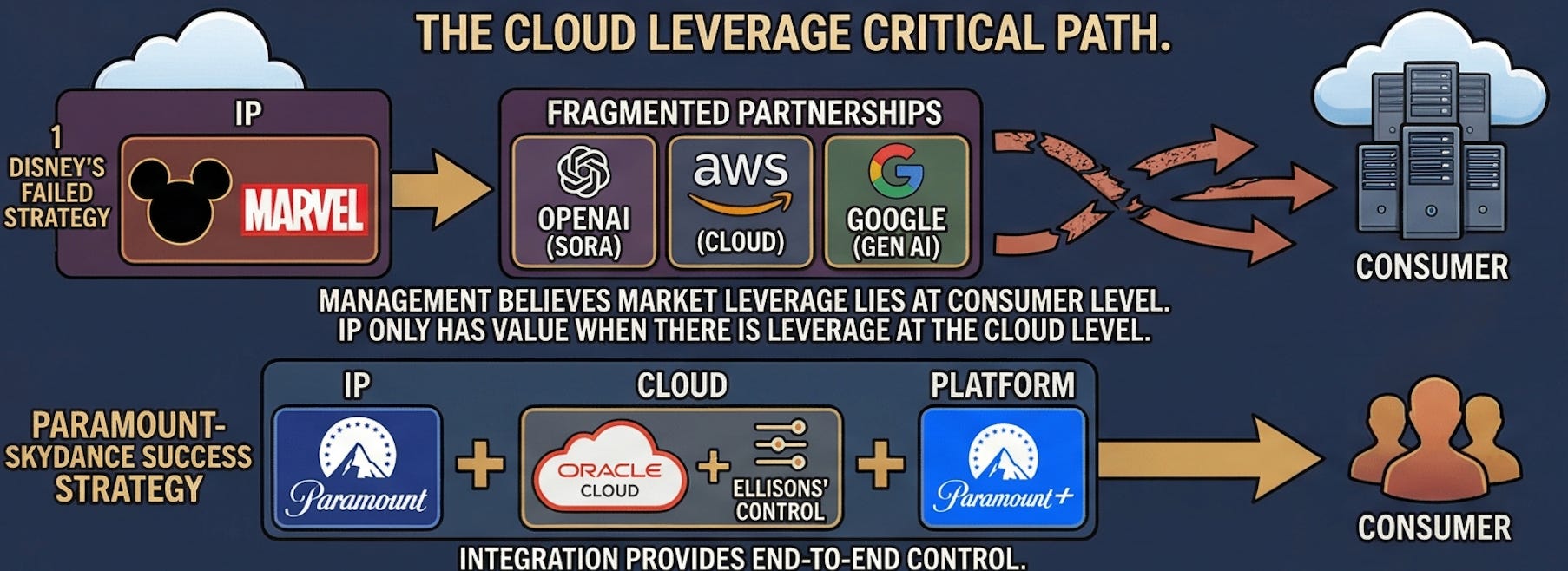

This outcome confirms my original concern from last November about Disney’s partnering with OpenAI instead of a company that owns a cloud solution. Disney management “believes it can have market leverage at the consumer-facing level. But, in the emerging marketplace, IP only has value to consumers when there is leverage at the cloud level.” The cloud is where AI models are trained on that IP, where derivative content is generated from it and where third-party distribution channels can pull the content.

Paramount Skydance and Oracle are quickly moving to build the cloud infrastructure that creates leverage to protect its IP in the AI era. Disney lacks similar available solutions. Instead, it has fragmented partnerships (OpenAI for Sora, AWS for cloud, Google for generative AI) that prevent the end-to-end control which Paramount Skydance achieves through the Ellisons’ control of both companies.

All coverage of this news has missed a crucial additional detail in the story: Disney sent Google a cease and desist letter on the same day as its OpenAI partnership announcement. Iger told CNBC “[W]e’ve been aggressive at protecting our IP, and we’ve gone after other companies that have not honored our IP, not respected our IP, not valued it. And this is another example of us doing just that.”

The message to the market was clear: Google was a bad actor and OpenAI was a good actor. Because OpenAI was a good actor, Disney shareholders would see upside in both operational cost-savings from the deal and value in Disney’s share of OpenAI’s growing market value. The message was re-emphasized with its recent cease and desist letter to Bytedance, the owner of the viral generative AI platform Seedance.

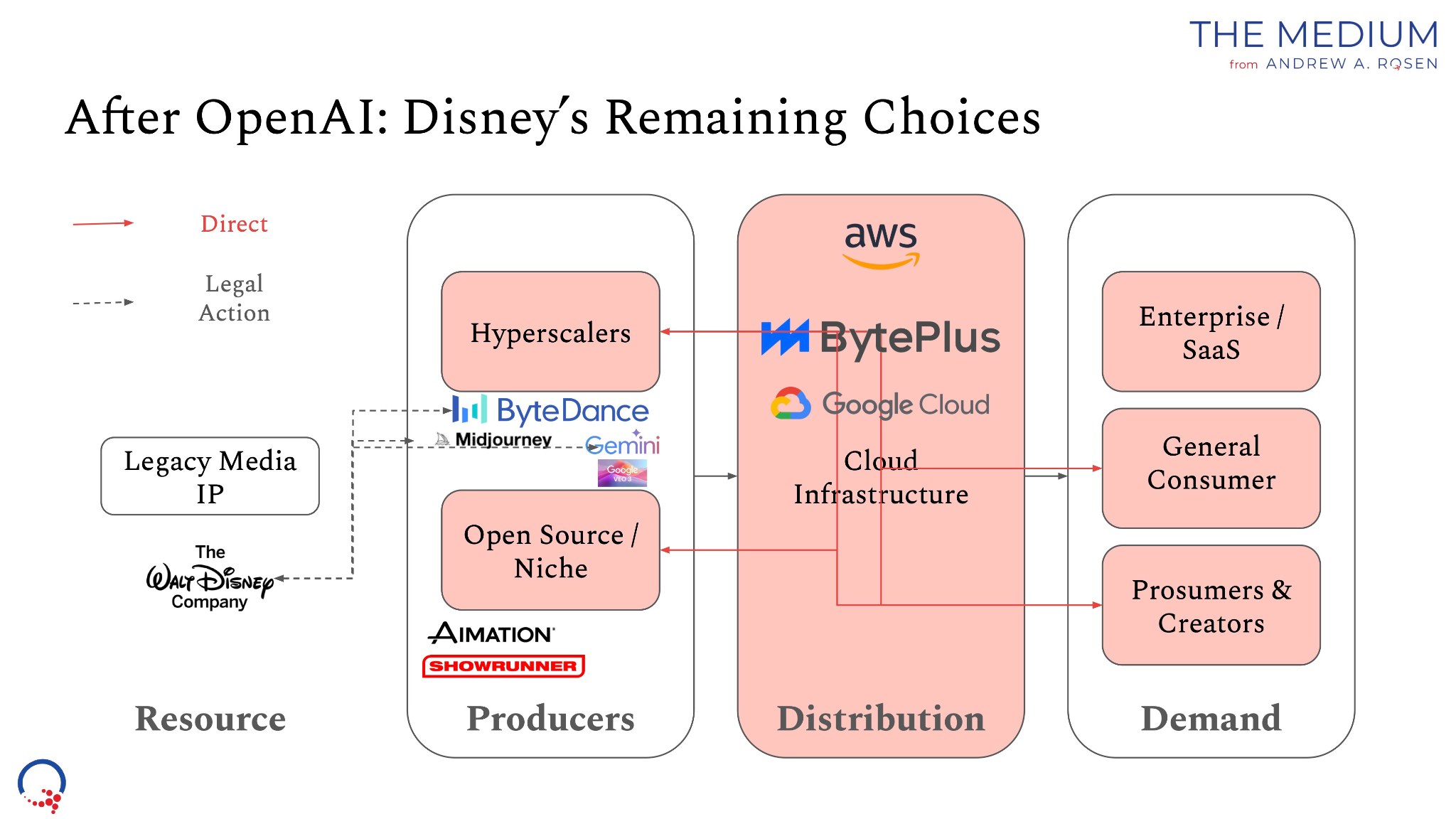

Google and Bytedance are now Disney’s only remaining “dance partners” in the hyperscaler world. Working with either or both will require walking back legal action and an agreement for cloud training. There is also Midjourney, which Disney sued alongside Universal last June.

Its other choices include smaller open source and niche platforms—I have previously highlighted Fable Simulation’s Showrunner and AiMation as examples. Runway seems to be off the table, recently raising $315 million in Series E funding to pivot away from Hollywood and “pre-train the next generation of world models and bring them to new products and industries.”

Whatever it does, its choices are more limited than before because it has opted for litigation over a cloud training partnership strategy.

Misalignment

The diagram above maps the AI content market onto the structure of the global beer industry. To remind you:

Oligopolies (AB InBev, Heineken) = Hyperscalers (OpenAI, Google) with large foundational models

Craft breweries = Open-source / Niche AI model makers

Distributors = Cloud platforms

Homebrewers and enthusiasts = Prosumers and creators

I previously wrote that the beer market analogy is valuable because it shows how oligopolies adapt when enthusiasts get access to quality equipment.

That same dynamic is true in AI but at 1,000x the scale—there are 10,000 craft breweries worldwide but over 20 million Midjourney users. That means both creators and smaller platforms have an outsized impact in the AI marketplace relative to homebrewers and enthusiasts in the beer marketplace.

The key difference between the two marketplaces is that post-Prohibition-Era state laws prevent beer companies from owning distribution. That means a brewery can make the best product in the market and still fail if it does not have distribution. But in the AI marketplace, distribution can come in the form of either a streaming platform and a cloud solution where models are trained, content is generated and derivative works emerge that can be distributed wherever the cloud solution permits.

So Google can own Gemini, Google Cloud and YouTube, and the Ellisons can control Paramount, Oracle Cloud and Paramount+. Owning the distribution creates leverage over every platform—niche, open source or hyperscaler—that needs cloud infrastructure to train models and generate content using owned and original IP.

I argued last November why Disney should focus on partnering with companies in the Distribution part of the marketplace instead of the producers:

“Disney should focus on finding its Oracle equivalent—a cloud partner with the aligned incentives that come from shared ownership (like the Ellisons have with Paramount and Oracle), providing end-to-end integration from IP licensing through infrastructure to AI tools. Because leverage in the cloud translates into leverage at both the levels of generative AI tools—both from hyperscalers and open source and niche tools—and creators and prosumers using generative AI apps.”

That partner is harder to find now because Disney spent six months signaling that litigation was its preferred strategy. Disney had also relied on OpenAI to help it tell a story of AI driving operational cost-efficiencies. That story is lost.

Disney now finds itself fundamentally misaligned with both Wall Street and the broader AI marketplace. It is an unfortunate but poetic ending to Iger’s tenure—beginning with the video iPod, he found success in pivoting Disney’s brand to digital media by using IP as leverage over new technologies.

This strategy became “long in the tooth” after Disney’s Maker Studios acquisition failed in 2016. The OpenAI failure bookends the arc of that strategy and leaves an unfortunate mess for new CEO Josh D’Amaro.