Nielsen's "The Gauge" Is Broken. Big Changes Loom For The $1 Trillion Ad Market.

The traditional media value chain is collapsing at every node, The dollars leaving that system may not go to another platform. Creators building IP with brands will reap the rewards.

Author’s Note: This essay is free for all subscribers

Three developments from this past month reflect a weird moment for the $1 trillion advertising marketplace I wrote about in January.

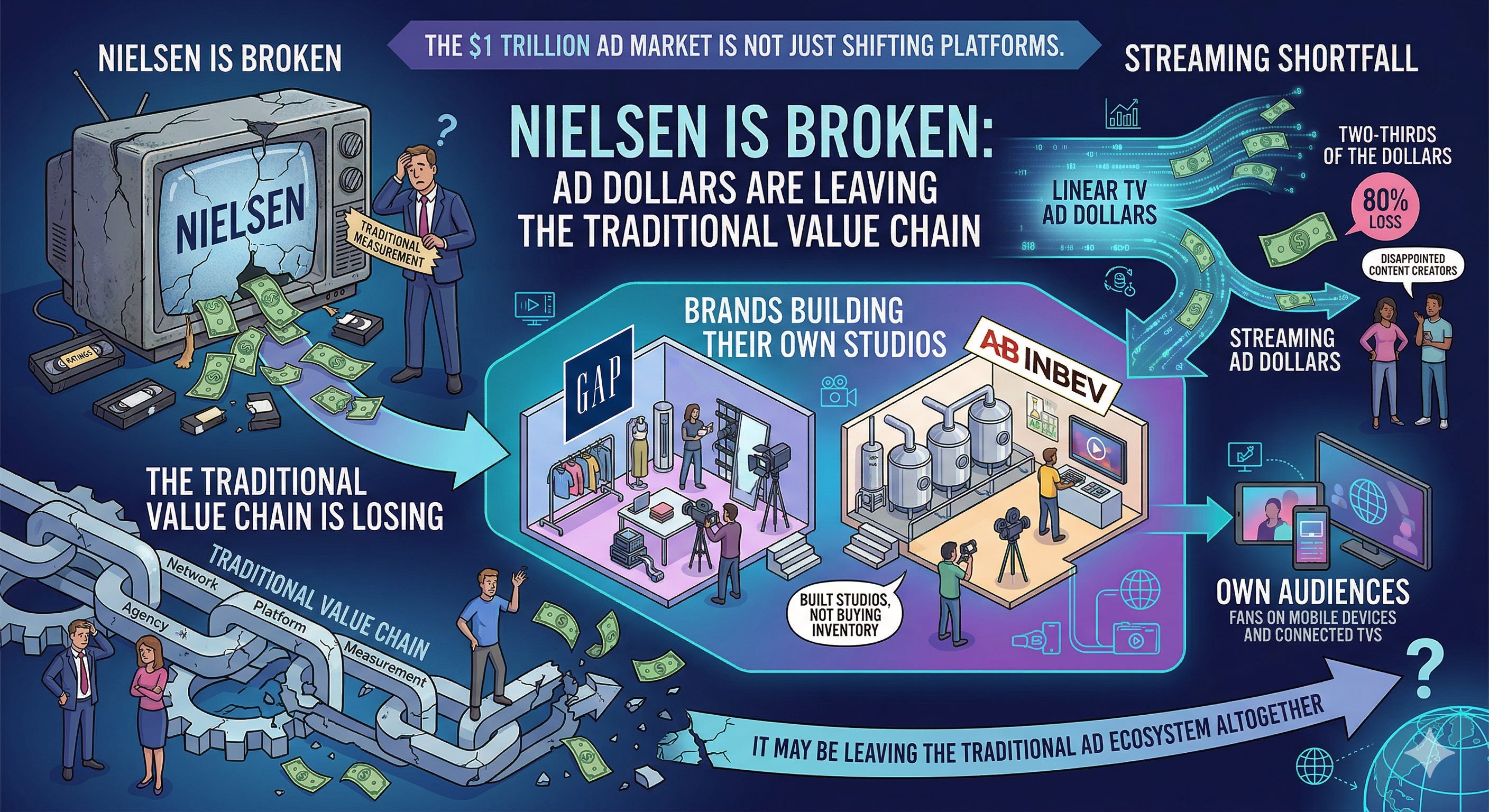

First, the video market has become a zero-sum game with a shrinking ceiling. Streaming is pushing more consumers to cheaper, ad-supported tiers but only recapturing two-thirds of ad dollars being lost from linear, according to research firm MoffettNathanson. The rest of those ad dollars are leaking to YouTube and other digital platforms.

Second, Variety and The Wall Street Journal both reported that Nielsen’s popular “The Gauge” may be providing an inaccurate lens on the video marketplace. Nielsen had previously drawn estimates entirely from its own volunteer panels. In recent months, it began warning clients that “its broadcast and cable TV figures could see a boost in February after it began using a study from the industry’s Advertising Research Foundation to inform its estimates of the demographic groups in U.S. households and the technologies they use to watch TV.”

In response, Nielsen has yet to release The Gauge for February 2026. Streamers are pressuring Nielsen to delay the report because of this ARF methodology. The annual upfronts and newfronts events—where broadcasters and streaming platforms pitch upcoming inventory to marketers and ad buyers—start soon, and the industry does not have reliable data on where audiences actually consume content.

Last, Jason Zada—founder of entertainment studio Secret Level—argued in a recent essay that “the old playbook” of “interrupt, target, repeat” for TV and streaming advertisers is “getting harder and more expensive to run every year.” This model is also “always late”—”The gap between ‘this is culturally relevant right now’ and ‘our campaign is ready’ has always been the dirty secret of the industry.”

The message from all three different market signals: The traditional media value chain—produce content, attract audiences, sell advertising against those audiences, measure with Nielsen—is collapsing at each node.

Back to the $1 Trillion Ad Marketplace

In January I argued that the new AI advertising infrastructure being built—scene-level targeting, AI production tools, programmatic efficiency—”extracts value from storytelling without distributing value to storytellers.”

I added:

“The differentiation for monetizing storytelling is not quality—it is operating capabilities. For fat tail creators, that means infrastructure to monetize the moments algorithms surface. For successful mid-tail creators like TBPN, it means infrastructure to monetize without algorithmic ad targeting at all.”

Zada argues that in this market, the barrier is lower for brands not to just become creators but to “develop original IP, put it in front of an audience, learn in real time, and iterate — the same way a tech company ships and improves a product — rather than betting everything on one expensive, slow-moving campaign.”

The infrastructure of monetizing moments that algorithms surface favors this model: “The fear of the big swing gets a lot smaller when you can take fifty fast swings first, each one more informed than the last.” Agencies like Secret Level and AI storytellers working for brands are the ideal partners for this model.

Two Questions for Upfronts & Newfronts

This leaves two open questions for upfronts and newfronts.

First, what will happen to legacy media advertising spend?

Both Linear TV (-3.3%) and broadcast (-2.5%) Upfront spending fell last year, while streaming surged (13.9%). Whatever the revised Gauge says about streaming, YouTube is positioned to capture more. Measurement is broken. The upfronts are becoming less relevant—not only because key Nielsen data is unreliable but because there is an emerging alternative that does not need the sellers.

Second, if brands reduce spend with linear and streaming, will those dollars shift towards the creation of original IP?

If brands follow Zada’s model and build their own entertainment infrastructure, the dollars will not shift from linear to streaming or from streaming to YouTube. Instead, they will leave the traditional advertising value chain altogether. The upfronts are selling inventory inside a system that brands are beginning to build around.

A Hidden Catalyst

Zada’s proposal also connects to something I wrote in February:

“A Cambrian explosion of creators outside Hollywood may be coming. But the path to building and monetizing original IP requires physical infrastructure, legal literacy or an audience at scale. Most AI storytellers stand at the fork possessing none of these.

The successful path with brands has a lower bar—the skill set to orchestrate creative across multiple tools and a few days of schedule bandwidth.”

The implication is that Nielsen’s failure to measure audiences accurately is creating the conditions for brands to stop relying on third parties to create the moments to connect with those audiences. This will be a catalyst for generative AI creators like Zada to reap the gains.