Monthly Series: Netflix Users Pay Once a Month. Drama Slop Users Pay The Equivalent Every Week.

AppMagic's Mobile Market Landscape Report sheds new light on three new and dynamic business cases of disruption in digital media

[Author’s Note: This is the second in a monthly series where I update past data from AppMagic on three new and dynamic business cases of disruption in digital media. You can read the first here.

Both are free for all subscribers.]

Last month AppMagic released its Mobile Market Landscape Report.

They shed new light on the three themes from the last Monthly Series with AppMagic data:

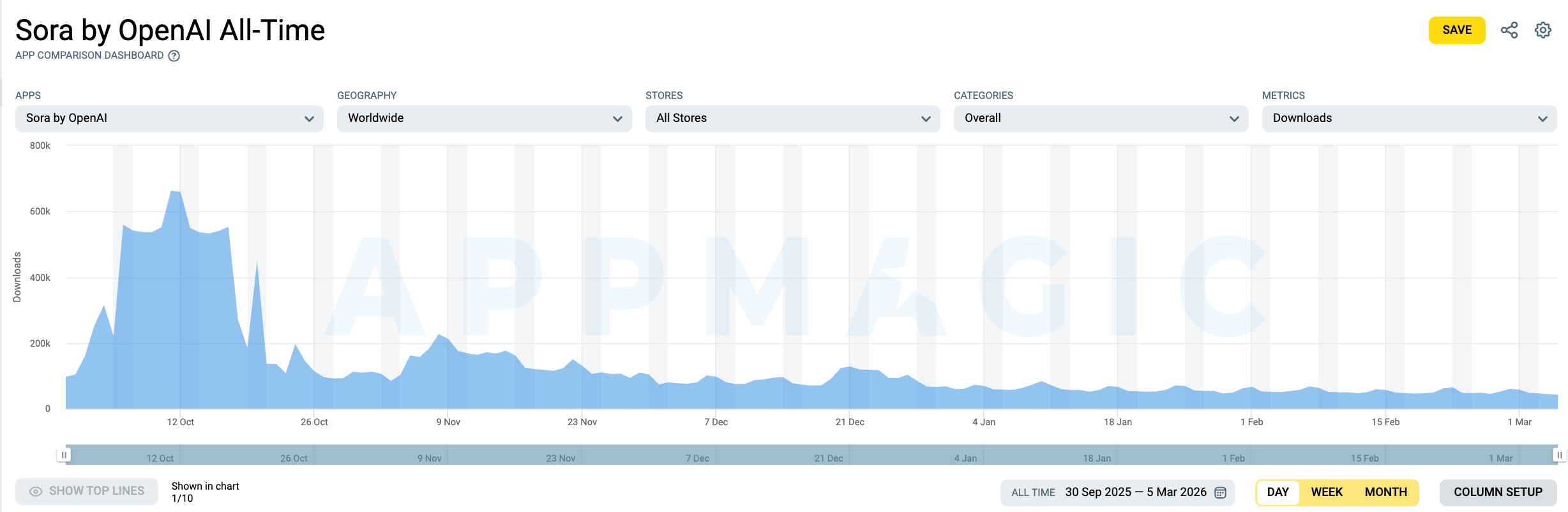

The dropoff in downloads of OpenAI’s Sora App

Netflix’s pivot in its mobile games strategy

The Rise of “Drama Slop” Apps

NOTE: A reminder that AppMagic only tracks in-app mobile revenue in the App Store and Google Play.

Generative AI Apps (Sora + Chatbot apps)

Key takeaway: User retention is falling, which means the AI platforms monetizing this attention are capturing value from a shrinking core of power users, not a broadening base.

AppMagic reported that the overall generative AI marketplace grew nearly 3x from 2024 to 2025 and is now a $3 billion marketplace. This marketplace includes Sora alongside OpenAI’s ChatGPT, Google’s Gemini and X’s Grok.

Revenue for these apps grew faster than downloads in 2025—273.6% to 178%. ChatGPT is estimated to have generated $2.33B on 990M downloads (+193% YoY) and Google Gemini hit 474M downloads (+381%).

However, user retention has decreased. AppMagic observed the largest drop in the first days of user life (–6.2%), while mid- and long-term retention decreased by 3.9%–4.5%.

This is all occurring against the backdrop of apps surpassing games in mobile revenue for the first time in September 2025. Generative AI platforms increasingly monetize attention through recurring revenue while the games selling discrete entertainment experiences fall behind.

This outcome reflects a market dynamic I identified back in January: When algorithms increasingly define which moments matter and platforms build scene-level precision to monetize them, how do individual storytellers capture value?

My answer: “In the Algorithmic Era, storytelling creates these moments, but infrastructure captures the value.” ChatGPT is infrastructure. Sora at 20.7M lifetime downloads and flat growth—only 2M additional downloads in roughly two months—is selling intermittent, interactive creative experiences in a market that rewards recurring subscriptions.

Netflix’s Pivot Away From Mobile Games

Key takeaway: AppMagic plus other data shows stalled growth in the mobile market. Netflix may have seen many opportunities four years ago, but its pivot suggests it sees fewer now.

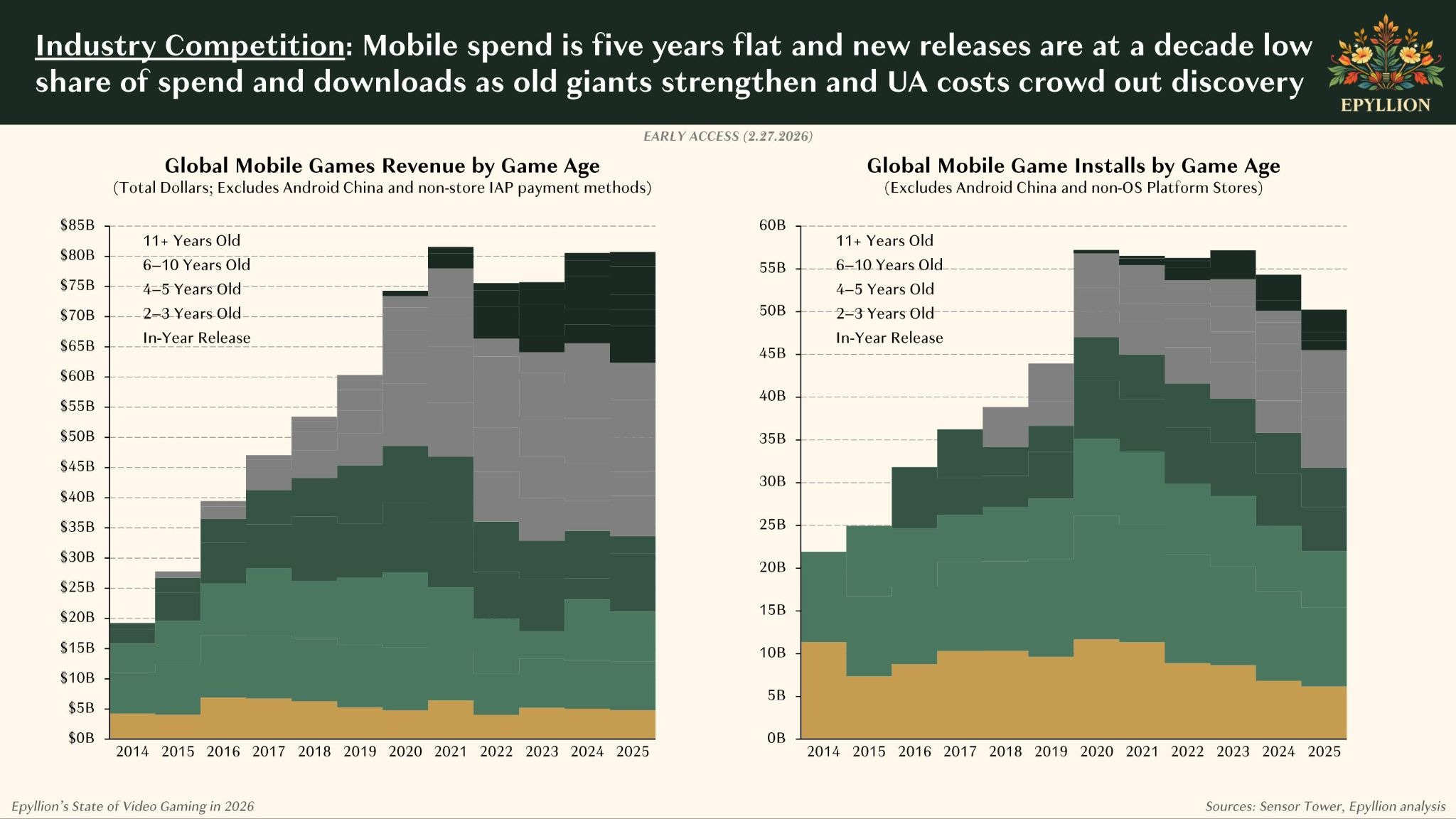

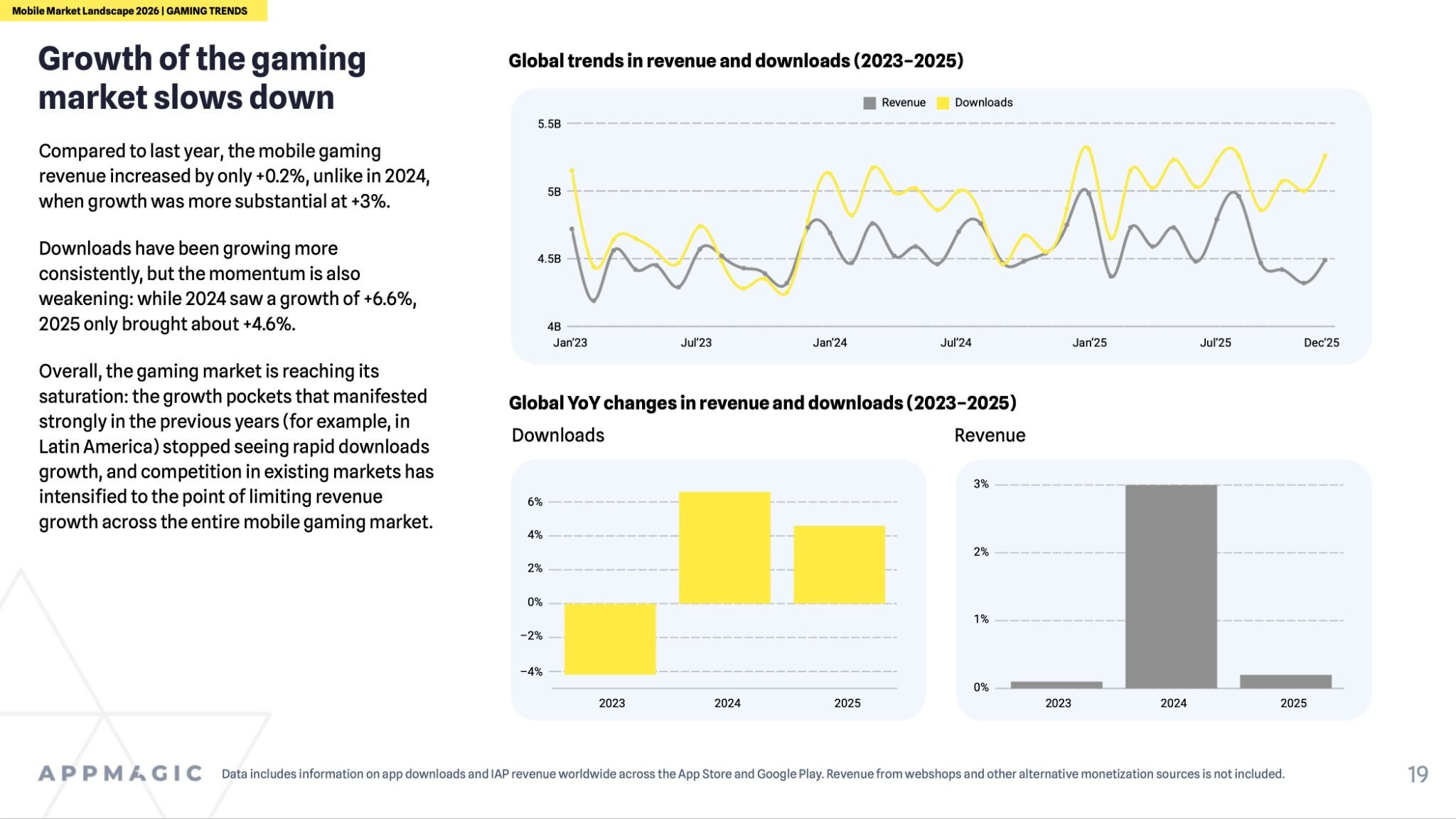

The gaming market is reaching saturation, suggesting Netflix’s retreat from mobile games was impeccably timed.

Revenue grew just 0.2% YoY (down from 3% in 2024). RPG revenue dropped 16.6%. Strategy grew 16.1%, driven by 4X titles like “Last War: Survival” and “Whiteout Survival” where $99 offers generate roughly 30% of revenue. LATAM—which was the growth story a year ago—is now declining in downloads across Colombia, Peru, Ecuador and Argentina.

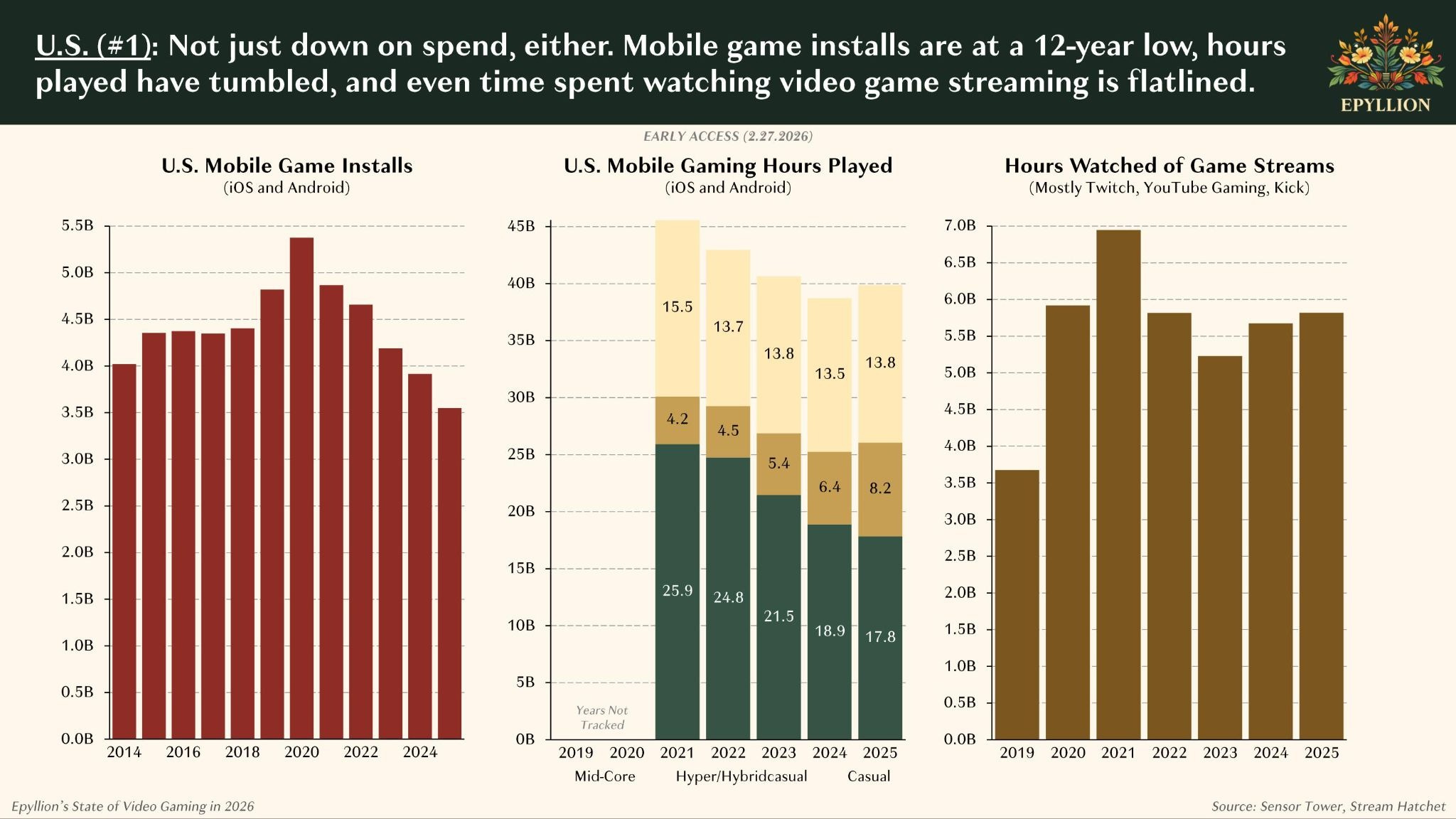

Matthew Ball’s Annual State of Video Gaming deck shed additional light on why the mobile gaming market is flat. It highlights broader declines in user engagement and revenues of games across demographics (slide one). It also points to declining hours played (in the U.S.) and livestreams of games globally.

Given these trendlines were emerging in 2022, why was Netflix so bullish on mobile games over the past four years?

The logic was sound. The internet is interactive. Netflix’s platform captures value from interactivity with media. If Netflix could capture additional interactivity cost-effectively, it would reduce churn and drive growth in certain markets, too.

But the global market stalled. Revenue growth collapsed from 3% to 0.2%.

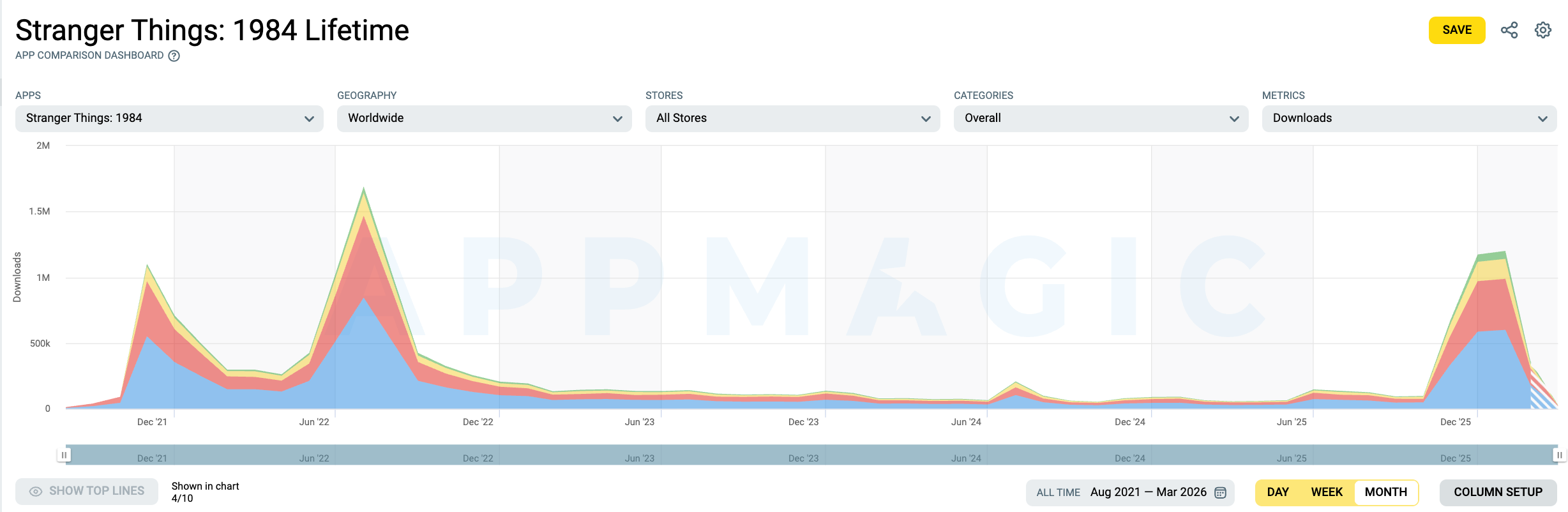

Particular game formats are more popular than the ones Netflix has bet on. Netflix’s “Stranger Things: 1984” is a casual adventure game. AppMagic’s report shows downloads of the adventure format for hypercasual games were -30.7% year-over-year. We also see from AppMagic’s download data that downloads of “Stranger Things: 1984” were -29.7% from 2022.

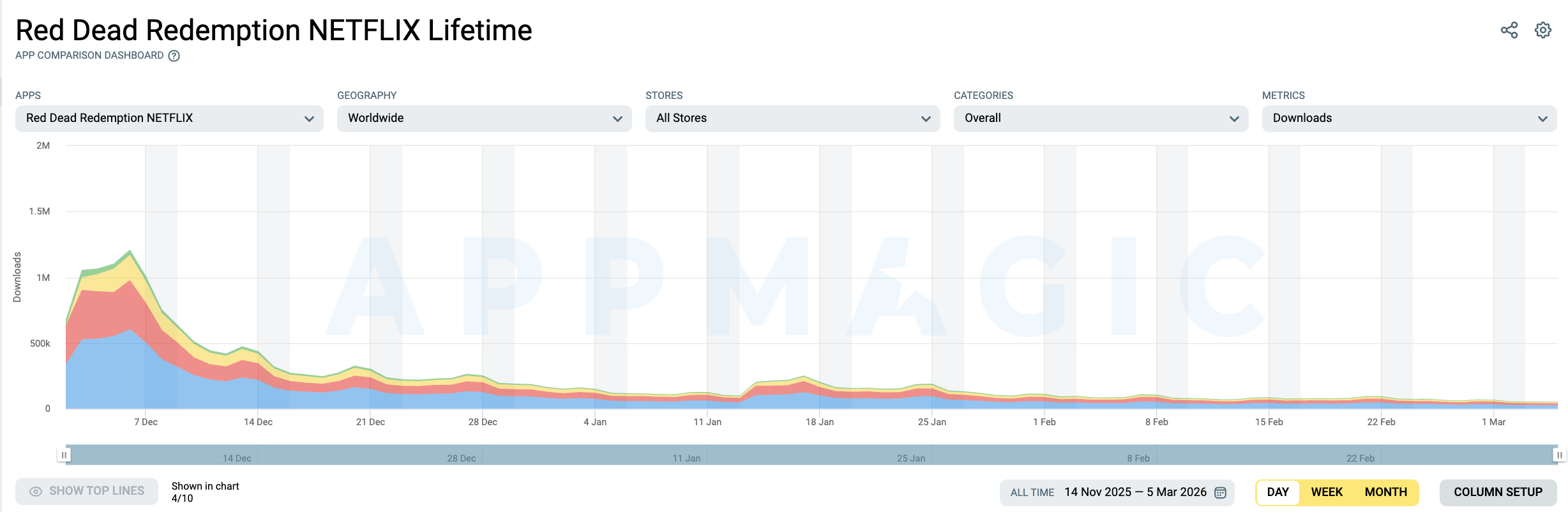

It recently bet on the popular midcore format—meaning, playable in a relatively short period of time while retaining some complexity—with action-adventure title “Red Dead Redemption”. That should be a better performing bet, according to AppMagic data. Downloads of Adventure titles are up 7% between 2024 (163.3M) and 2025 (176M). Also, downloads of Action titles are effectively flat year-over-year at 2.2B (-1.4%).

However, since its release, downloads of the app suggest steadily waning interest. Even with smarter market bets, the data points to obvious disconnects in Netflix’s mobile business model—it bundles games into a subscription rather than selling them directly. At over 330 million members, it is hard to imagine how 10 million downloads–and slowing—are moving the needles on engagement and reduced churn.

This data both justifies its recent pivot and raises more questions.

The Rise of “Drama Slop” Apps

Key takeaway: Investors wonder how Netflix will defend itself against Drama Slop on iOS and Android after this report.

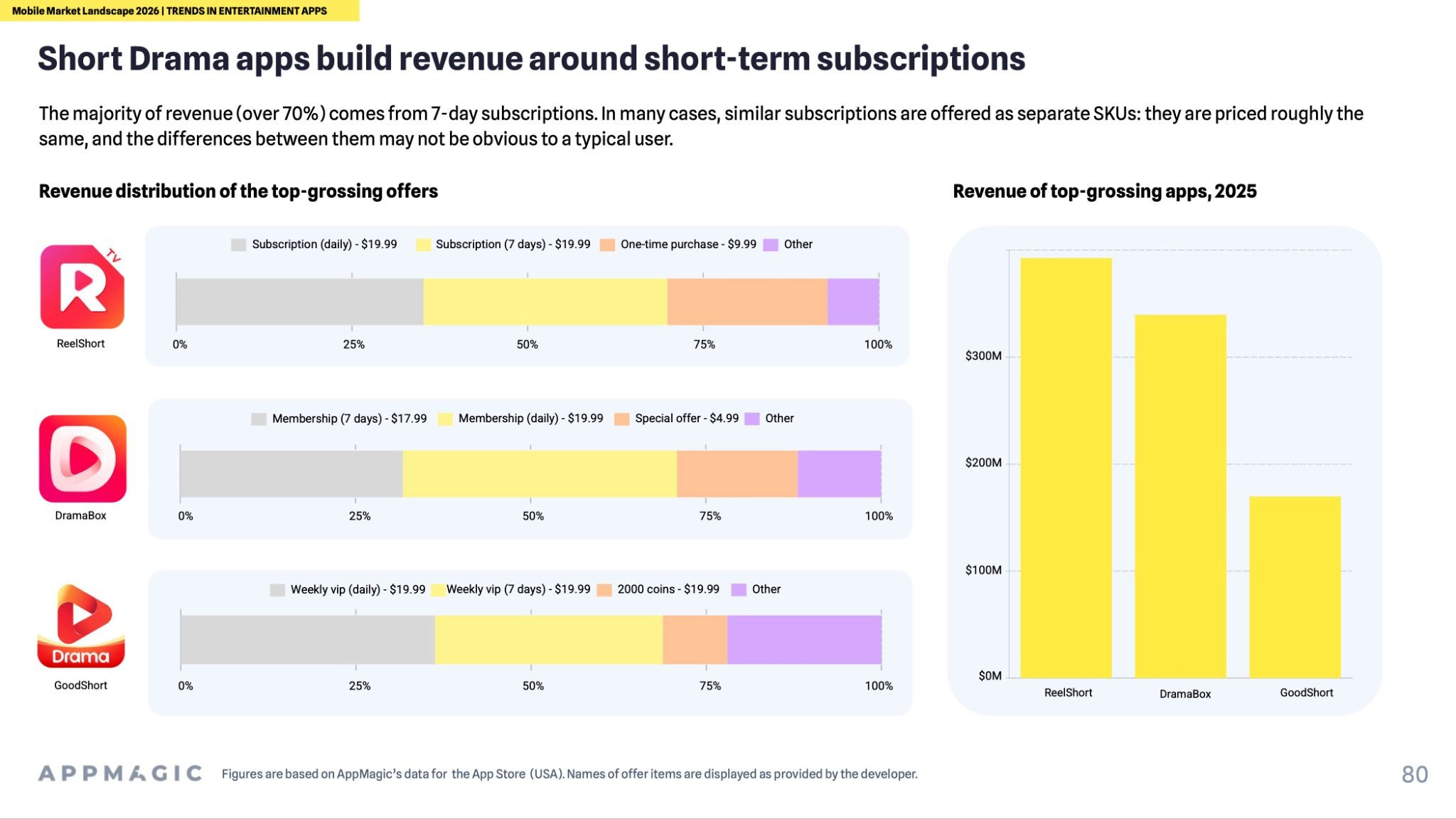

Short Drama aka “Drama Slop” as a category hit $1.8B in revenue (+93.5% YoY) on 2.1B downloads (+279.5%). The market grew nearly 4x in downloads in a single year. ReelShort and DramaBox were the top two grossing Short Drama apps of 2025, more than 2x the size of their third place competitor GoodShort.

The report also highlights how the segment is showing a “clear stability” phase after a 1,000%+ revenue spike in 2024. Monthly revenue now holds steady between $145M and $160M even in weak months. And monetization runs on 7-day subscriptions at roughly $18–$20, with over 70% of revenue coming from that single offer type.

The cost of a Standard monthly Netflix subscription is spent weekly on these apps. This data point strongly supports my argument from last July that the Drama Slop model has “increasingly more value to consumers than Netflix’s walled garden”.

ReelShort and DramaBox together pulled roughly $700M in 2025 from a format that did not exist three years ago. The challenge for Netflix is not only that this new format is competitive with the 27-year-old incumbent in such a short period of time, but that its weekly and monthly spend suggests consumers value the new format more. There is a meatier story to the rise of “Drama Slop” apps in the rankings than just their outperformance of Netflix on AppMagic’s download charts.

Investors have growing questions about the strategic direction of Netflix’s business, especially after its failed bid for Warner Bros. They will wonder how Netflix will defend itself against Drama Slop on iOS and Android after this report.

Final Takeaways

AppMagic's Mobile Market Landscape Report added sheds new light on three new and dynamic business cases of disruption in digital media:

GenAI platforms capture recurring revenue despite falling retention

The mobile gaming market and Netflix’s bets within it have stalled

Drama Slop consumers spend in one week what they could spend on a Standard monthly Netflix subscription.