People Inc. Is Partnering With the Wrong Part Of The CPG Marketplace

Why licensing to competing SMBs beats picking an incumbent CPG partner.

[Author’s Note: This essay is free for all subscribers.]

Last October, I wrote that intellectual property holders in media and entertainment “risk being fragmented before they can fragment themselves.” Around the same time, People, Inc. Chairman Barry Diller described—in a podcast interview with Patrick O’Shaughnessy—a strategy his company now calls “INVERSION”. Rather than licensing its brands to CPG companies, People, Inc. would partner with them to build and own consumer products. Their best strategy is to fragment themselves.

In a recent podcast interview, CEO Neil Vogel framed this approach to fragmenting People, Inc. around “permission”:

“Brands that people love and care about, they’re going to be permissioned to do different things. When we figure out what they’re permissioned to do, we’re going to do those things and that’s how we’re going to connect with audiences and that’s how we’re going to make money. And it actually works.”

“Permission” reveals the dynamic beneath “being fragmented before they can fragment themselves.” Even as platform disruption and an accelerating supply of creator-led products erode the value of publisher brands, People, Inc. still has talent and assets—first-party data, editorial relationships and advertiser trust—to identify a market need and build a branded product around it. Diller has touted a few initiatives: a Southern Living tea, a chef-driven product line from Food & Wine and a Travel & Leisure entertainment property with the cultural reach of “The White Lotus.”

However, there are two challenges to this. First, as I wrote on Monday, Meta, Google and Amazon are making it easier for creators and SMBs to build, market and sell products without a publisher in the value chain. They are “flattening” both production and distribution models—collapsing financial, legal and technical barriers to entry—enabling more competition that will “fragment” People, Inc.’s portfolio of companies. Vogel conceded this reality in his interview on Channels with Peter Kafka: “we’ve already lost more than half of our referrals from Google”. As a result, “40 of our brands don’t matter, about seven or eight of them matter.”

Second, generative AI platforms like Sora and Seedance 2.0 are demonstrating how quickly brand identity can be replicated by producers who have no stake in the original. INVERSION responds by maneuvering around that erosion. Rather than defending brand value in channels where it is under pressure, People, Inc. bets that brand equity can be converted into physical product demand before it depreciates further.

Given Diller’s ambition for INVERSION to build “a giant company,” and given data suggesting giant CPG hits have been rare in the past decade, brand equity and first-party data alone are not sufficient. A difficult environment for incumbents is getting harder faster.

The Real Question: Viability

The more immediate question is not whether People, Inc. can produce a giant hit but whether it can produce a viable one.

“Viability” implies a product that generates an annuity on existing brand equity. “Giant”implies a product with compounding returns, deepening the audience relationship with every sale and building an asset worth more than the brand that launched it. Analysis of 301 CPG breakout brands by CPG brand strategist Matt Alldian points toward viable, not giant, as the realistic outcome for People, Inc.

That market logic points to a deeper dynamic. People, Inc. is an incumbent media company. It seeks to partner with incumbent CPG companies to protect and extend the life of its brands. Both must compete with a growing supply of SMBs empowered by technology companies with massive advertising reach.

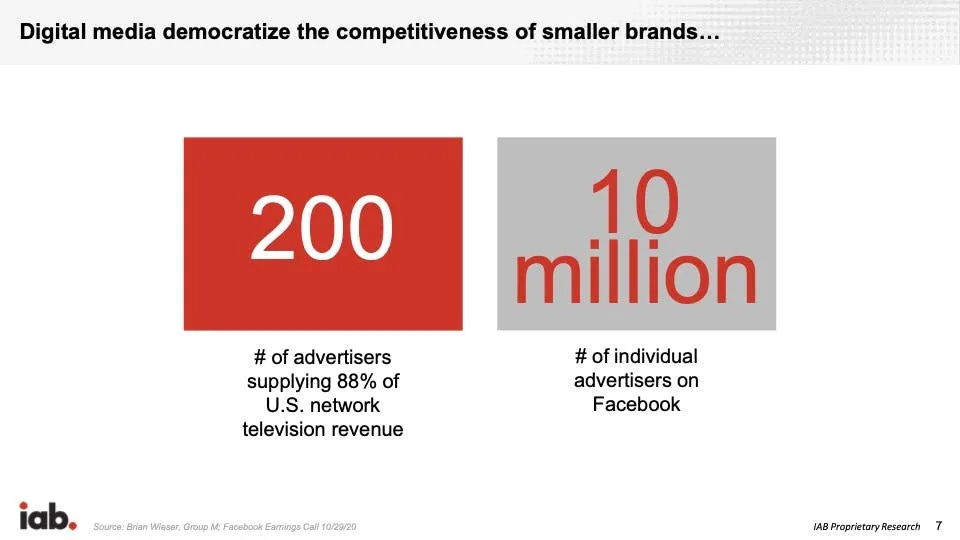

We have seen this dynamic before in the Interactive Advertising Bureau’s “The 200 vs. The 10 Million” framework from 2022. The 200 were the limited group of advertisers who supplied 88% of US network TV revenue. The 10 million were the emerging SMB advertisers on Facebook and Google. Platforms that bet on the latter made the better long-term play, and legacy media companies are playing catch up. Instagram now reports that over 200 million business accounts worldwide are posting videos and photos.

Recent earnings calls suggest that number will only keep growing. Amazon CEO Andy Jassy told investors last week that the AI tools make it “so much faster and so much easier” for SMBs and predicted there will be “a lot more advertisers with the rise of what’s happening in AI.” Google SVP and Chief Business Officer Philipp Schindler told investors on its Q1 2026 earnings call that AI-driven Search advertising campaigns enable SMBs to reach customers “at a scale that really wasn’t possible even a few years ago.”

The implication is clear—more SMBs with more tools will compete directly with both media incumbents offering products and CPG incumbents. With traditional TV inventory declining and streaming advertising fragmented across multiple Smart TV operators and streaming services, the incumbents will have less leverage over the rest of the marketplace. Kraft Heinz’s new CEO Steve Cahillane recently admitted as much to the Wall Street Journal: “I think we took for granted that brands would always stay relevant with consumers, and they don’t, no brand does.”

Reach is not Resonance

A media brand product play that lacks intentional audience building monetizes existing brand equity—an annuity on a depreciating asset. A creator-led brand with genuine audience resonance compounds, because every piece of content deepens the relationship that drives purchase.

People Inc. has reach and its first-party data (via its AI ad targeting product D/Cipher) can identify consumers for whom the brand resonates. The harder question is whether any of its brands have the depth of relationship that converts to purchases from fan bases—and not just a one-time trial driven by brand recognition.

Any partnership with a CPG incumbent begins with incompatible survival modes. A media brand survives on audience trust and monetizable attention—a niche of loyal, paying readers is a viable business. A CPG brand survives on shelf velocity and distribution coverage at scale. Under market pressure, both incumbents will optimize for their own survival in opposite directions.

Three outcomes are possible once a product finds resonance:

A viable product creates an annuity—steady revenue from a loyal niche that licensing alone would not capture, with both parties content to maintain the arrangement.

A hit product creates a revenue spike, but the shelf life of breakout CPG brands is shortening—what looks like a compounding asset may be a one-hit wonder that fades before it can become the foundation of anything larger.

A “giant” product generates sustained compounding returns and consumer retention over time, but Alldian’s data suggests this is the exception and not the rule. It also shows creators and brands with highly targeted products are best-positioned to succeed.

In the first scenario, People, Inc. has a revenue stream but not a company-defining asset. In the second, it needs to have a larger pipeline of products. In the third, the partnership structure that enables INVERSION may be the very thing that prevents it from reaching Diller’s ambition.

It makes one wonder whether People, Inc. may be better off licensing its IP to multiple SMBs and letting them compete for the best consumer product.